Spanish regional banks: from reflation to deflation trade

In early 2018, we warned investors (see our presentation “_Reflation trade and other myths_”) that the reflation trade behind the banking sector’s recovery was misplaced and that Spanish banks were particularly exposed. As a consequence, the capitulation of consensus expectations did not come as a surprise to us. However, in our view, the recent indiscriminate sell-off of Spanish regional banks has translated into excessively discounted valuations providing above COE potential returns.

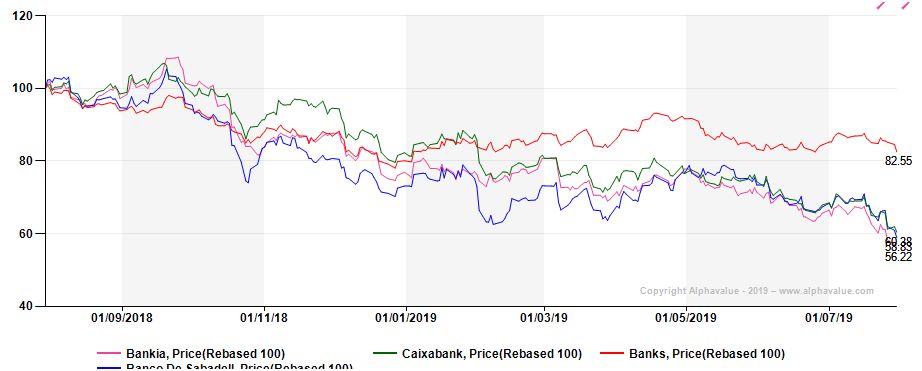

The three Spanish regional banks we cover (BKIA, CABK and SAB) rank among the five worst performers within our universe ytd, with share price corrections ranging from 17% to 26% while the sector is up by 6%.

Spanish regional banks vs AV banks (rebased)

Source: AlphaValue

The disconnect with the rest of the sector began in early 2019 and it is interesting to note that the three stocks have moved in tandem since early June, reflecting what seems to be an indiscriminate sell-off. The usual suspect behind the latter evolution is undoubtedly deflation as Spanish banks are well-known for having loan books largely indexed to the Euribor.

Overdone business models’ interest rates sensitivity

We know that this not a consensual view, but we continue to argue that the alleged sensitivity of banks’ business models to interest rates is largely overdone as confirmed by most of the tests performed by academics, central bankers or quant departments. This myth is based on the misconceived view that deposit banks would perform maturity transformations.

This is wrong. If deposits are a liquid claim, their maturity equals that of the loans from which they have been created! More generally speaking, like for any industry, banks’ margins are driven by competition, not by the evolution of the cost of doing business. Banks as service providers, try to secure a stable margin over managed assets, passing any change in rates to customers. Such adjustments are not frictionless but hedging is here to help.

ECB’s limited margin of manoeuvre

True, negative rates do not correspond to normal conditions. If they have been passed on to institutional and corporate clients (through increased fees as Spanish banks are not allowed to charge negative rates), banks have been reluctant to impact SMEs and individuals which enjoy lesser alternative investment choices. However, there is little doubt, as exemplified by the increase in Swiss mortgage yields in 2016, that banks will eventually search ways (increased tariffs on services or higher loan yields) to offset the impact of negative rates when and if they begin to really bite. For the time being, as stated by the ECB, the bottom line impact is not obvious as it is offset by hedging or a benign cost of risk.

As negative rates are equivalent to a rate increase as soon as they cannot be fully passed on to customers, we believe that the ECB’s margin of manoeuvre to cut rates further is largely constrained. Last but not least, the TLTRO 3 will be of reduced help as not only the rate has been reduced but also drawings from Spanish banks are likely to be significantly reduced as their liquidity has largely improved and they fear to be stigmatised.

Growth does not matter

Deflation comes with stagnating balance sheets. As long as the latter do not shrink, requiring staff cuts, this is not an issue to valuation. Indeed, contrary to non-financial companies, banks’ capital employed is directly determined by activity levels. In other words, slower expansion immediately releases capital that can be returned to investors. Last but not least, as most banks do not beat their cost of capital, it reinforces the lack of valuation’s sensitivity to growth.

Limited pension fund exposure

ROE has proven to be a poor value creation metric. Indeed, value creation is also impacted by non-P&L items (FX, pension funds, unrealised capital gains, etc.) and by the evolution of capital consumption.

Spanish regional banks have limited exposure to FX and pension funds, providing a safe profile in the current environment.

Non-sense IRPH litigation

Spanish banks are waiting for the ruling of the European Court of Justice, which is expected in the second half of this year, on the use of the IRPH index (corresponding to the average rate offered by banks) for a portion of their mortgage books instead of the Euribor. As this index has proved less sensitive to the fall in interest rates than the Euribor, some customers have tried to claim opportunistically for the payment of the difference. Rebuked by Spain’s Supreme Court, they turned to the ECJ. A different ruling would not make sense in our view.

CaixaBank is by far the most exposed with €6.7bn of mortgages indexed to the IRPH corresponding to 3% of its loans, followed Bankia (1.4%) and SAB (0.6%). Some analysts have evoked heavy potential losses. We believe the fears are largely overdone.

Heterogeneous equity leverage

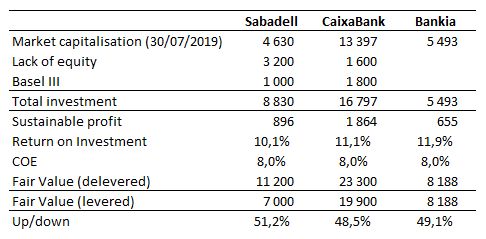

The capital position remains an important source of valuation metrics’ distortion. As a consequence, it is important to assess it properly. To make the exercise more complex, the pending impact of Basel III remains largely unknown.

Sabadell is a highly leverage bank. Not only its CET1 stands notably below the sector’s average but it presents a very thin distance to the MDA (individual threshold set by the regulator every year) and above all a particularly subdued stress-tested CET1 (6.1% vs a 10% average). The latter gap corresponds to €3.2bn of equity. Management does not disclose any guidance as regards Basel III. Based on the EBA’s latest impact study, we have retained a €1bn impact.

CaixaBank shows a decent distance to the MDA but a below average stress-tested CET1 (8.9%) pointing to a €1.6bn equity shortage. Again, the group does not provide any guidance as regards Basel III. We have retained a €1.6bn impact.

Bankia appears excessively capitalised on the distance to the MDA metric (+3.7%). Unfortunately, the group was not stress-tested. However, given its low risk business profile, we believe it would perform relatively well. Management expects Basel III to have a minor impact. We have considered that it should be absorbed by the excess capital and, consequently, cautiously consider that the group has no excess capital.

Sustainable profitability levels

We believe, more than ever, due to the low visibility on the macro-economic scenario, that banks’ valuations need to be assessed on the basis of sustainable profitability levels. Such levels can be inferred from the average historical return on assets or from a best-guess estimate when the data are not available (which is the case when it comes to Bankia and CaixaBank) or when the business mix has changed markedly.

As far as we are concerned, we believe that SAB’s profitability is sustainable as the group enjoys margins of improvement. We estimated that our projections for Bankia stand 15% above the group’s sustainable level. In our view, CaixaBank shows the strongest downside potential with projections standing around 35% above the sustainable level.

Again, we do not believe that low or negative rates can markedly distort across-the-cycle sustainable profitability levels as banks will adapt one way or another.

Our take

Below we propose a simple alternative way to assess fundamental valuations. Within this perspective, we use sustainable profits and derive a return on investment based on a normalised post Basel III capital structure. This enables us to compare the RoI with the sector’s cost of equity. Note that the latter is not derived from the CAPM’s formula but simply corresponds to the sector’s average return on investments. The latter stood at 7.5% in early 2018 (commensurate with the cost of Tier 1 debt) but has increased to above 8.5% today. We then deduct the excess/lack of capital and the expected Basel III impact to get the levered valuation.

Interestingly, the three studied stocks enjoy very similar upside potentials, confirming that they have suffered an indiscriminate sell-off. In our view, the depth of the valuation discount largely covers any unexpected risk.

For more research on Spanish banks : click here