AMS/OSRAM: Accretive deal, but stretched balance sheet at ST

AMS has reiterated its bid offer on OSRAM at €38.5/share (all cash), now being backed by two banks and having reshaped its industrial offer to satisfy the board. Obviously, this announcement came with AMS’s usually high volatility. We are cautious on the stock in the short term given the stretched balance sheet, but we remain positive on the company’ long-term perspective. We believe that the stock now embeds all M&A fears which were previously more like the sword of Damocles.

Following Allianz’s decision last week to refuse the Bain/Carlyle takeover bid at €35/share, AMS has reiterated its bid offer on OSRAM at €38.5/share (all cash), valuing the company at c. €4.3bn or c. 9.5x its EV/EBITDA. This proposition is 10% higher than Bain/Carlyle’s and represents a premium of 33% to the day before the PEs first offer.

This transaction is fully underwritten by a bridging loan from HSBC and UBS, and therefore a €1.5bn capital hike is expected to happen, fully underwritten by both banks. Post-operation, AMS targets a leverage ratio of 4.3x its EBITDA post-transaction.

The main offer period starts on 5 September until the end of September/beginning of October and the transaction is expected to be closed in H1 20 (subject to regulatory approvals). Between these two dates, ORSAM will hold an extraordinary general meeting to review the proposal.

AMS targets both cost and revenue synergies in excess of c. €300m.

What is OSRAM?

OSRAM has generated €3.5bn in revenue over the last twelve months from three segments; €1.5bn – 43% of revenues – from Opto Semiconductors (semiconductors and micro-modules), €1.1bn – 31% – from Automotive (Light source components and sub-systems) and €0.9bn – 26% – from Digital (construction & refurbishment project business and Electronic sub-systems). According to OSRAM’s last CMD data (in September 2018), the Opto segment is set to be the main growth driver and the most profitable activity (+10% revenue growth expected in the medium term with between a 23% and 29% adjusted EBITDA margin), while both Automotive and Digital are expected to grow more modestly (in the range of +3% to +7%), with profitability respectively of 9-11% and 5-10%.

Complementarity of products and diversification benefit

The combined entity is expected to reach €5bn in revenue with a double-digit growth profile and 25% adjusted EBIT in the medium term. The Digital business is expected to be phased-out to an “appropriate” third party. Given its growth perspective and profitability assumption, we can assume that a valuation between 0.7x and 1x its sales could be reached (OSRAM is currently valued at 1.15x on the market, according to Bloomberg), which could ultimately help AMS to deleverage the structure further.

We believe that this operation makes sense from a product perspective for AMS on Opto Semiconductor, since the OSRAM Emitters will complement the current ToF and VCSEL offer for 3D sensing.

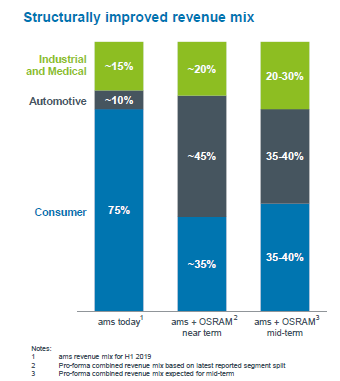

This transaction is also a way for AMS to diversify its activities away from the smartphones business and, more importantly, reducing its exposure to Apple (c. 40-45% expected in 2019) along with increasing content in the Android environment. We also appreciate the acceleration of its exposure to the Automotive market (Automotive Chip Market to enjoy the highest growth, according to Gartner, with a CAGR 2018-22 >10%), from c.10% today to between 35% and 40% in the medium term. This could provide a steadier streamline in cash flow going forward.

EPS accretive in year 1, but OSRAM will weigh on margins

Financially, AMS expects this operation to be EPS accretive in the closing year and to derive c. €300m cost and revenue synergies from the transaction. The synergy drivers will be on the COGS and opex (both at c. €120m) achieved in the first two years through footprint rationalisation in Asia and team optimisation (IT, marketing and R&D…). Also, the LED front-end production will be repatriated to Regensburg (Germany). We see this move as a positive point for the regulatory bodies and trade unions. On top of this, c. €60m is expected to be achieved thanks to the portfolio combination and the creation of new products.

However, looking at the current Bloomberg’s consensus for OSRAM, this currently targets an EBITDA margin for 2020 and 2021 below AMS’s (i.e. 11.1% and 12.9%). We believe that this will be a drag on the margin and, since synergies will take time to materialise fully, we expect the combined entity’s EBITDA margin for 2020/21 to be c. 24.4%/25.1%, down from 29% expected in 2019 for AMS standalone. For the same reason, we are also rather sceptical about the nature of EPS accretion from day one.

Financing and impact on leverage, tense in the short term

HSBC and UBS have fully underwritten the transaction with a bridging loan that will then be financed with: i) a €1.5bn capital hike (fully underwritten by both banks), ii) a €2.7bn debt issuance (expected rating in the BB area), and iii) €300m in excess cash. Post-operation, AMS targets a leverage ratio of 4.3x its EBITDA, and 3.2x in 2020 which should then fall to below 2x from 2021 onwards. We, however, highlight that these targets already integrate the synergies fully as if they were materialised immediately.

So, despite being more cautious than the company on its leverage ratio, we anticipate (if the operation is carried to its end) a higher leverage for 2020 (3.9x) which should then (all else being equal) trend down to 2x by 2021.

Need to convince the board and shareholders, not yet done

This transaction remains subject to regulatory approvals but also needs to be validated by@ i) the OSRAM board and ii) its shareholders with a minimum acceptance rate of 70%. While AMS said it has revised its offers, which now fully address all previous pitfalls pointed out by the board (industrially and financially), we believe shareholders’ acceptance will be the main issue. Indeed, the price offered by AMS has not changed since the previous offer and is just 10% above the Carlyle/Bain’s, which was viewed as undervalued by Alliance, OSRAM’s current largest shareholder.

Our take

All in all, we maintain our Buy rating, but we keep in mind that the stock will remain very volatile in the coming months due to: i) the sharp increase in leverage through 2019/20, and ii) the potential high exposure to the automotive market which is currently under the spotlight as demand has turned out to be weaker than previously anticipated for 2019. Our Buy recommendation is, therefore, taking more into consideration the long-term perspective of the company, with increasing FCF generation and managing to gain market share in the Android environment. Also, we believe that the stock now embeds all M&A fears which were previously more like the sword of Damocles.

Get full report on AMS/OSRAM : click here