Getinge reported strong Q1 21

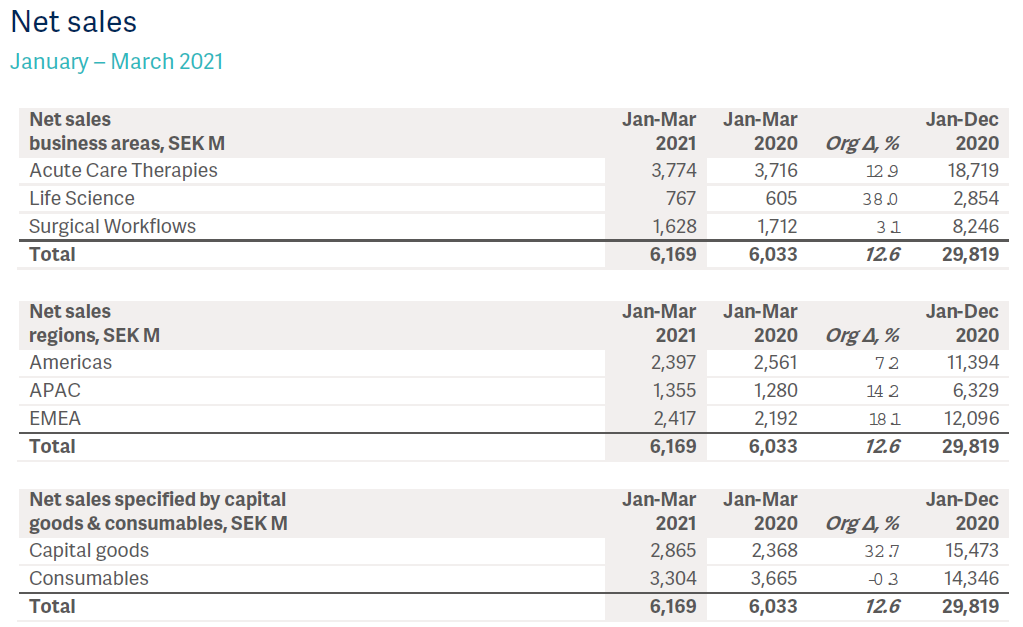

Getinge reported strong Q1 21 numbers, beating estimates. Sales were up 12.6% on an organic basis, driven by the strength in acute care (+12.9%) and life science (+38%). The order book decline (-22.8%) was expected given the exceptional order build-up in Q1 21. Profit margins (adjusted EBITA margin +650bp) were well ahead of estimates, thanks to improved cost controls.

FY21 guidance was unchanged (revenue of at least SEK27bn). We will upgrade our estimates to factor in the strong margin trajectory.

Getinge reported a strong Q1 21, beating estimates across the board. Sales were up 12.6% (to SEK6,169m) on an organic basis, driven by strength in acute care (+12.9%) and life science (+38%) with broad-based regional growth.

However, the order book (SEK 6,616m) was down 22.8%, which was expected given the exceptional order build-up last year, following the onset of the pandemic in Q1 21.

Interestingly, the firm’s margin expansion tracks ahead of estimates (adjusted EBITA/EBITDA margin +650/590bp), thanks to improved cost controls. FY21 guidance was unchanged (revenue of at least SEK27bn).

Analyse

Broad-based growth

The strong Q1 21 growth was encouragingly broad-based, with growth across all regions and business segments. As expected, growth was entirely attributable to the capital goods/equipment sales, a trend also seen over the last three quarters of 2020, thanks to the strong sales of critical care equipment (~50% of normalised ACT sales). As the momentum for Ventilators and ECMO normalises (in H2 21, provided we don’t have another pandemic flare-up), the higher margin consumables sales should gather pace.

Source: Getinge Q1 21 earnings release

Conservative guidance given healthy underlying growth

The order book decline (-22.8%) isn’t unexpected, given the strong order build-up seen in Q1 20 (with +47.2% order book growth). Nevertheless, the SEK6,616m order http://www.buyxanax.org/ book represents over 7% growth vs Q1 19 (3.5% annualised vs 2-4% long-term growth target), implying that underlying demand remains strong.

In the context of the strong underlying demand (+7%/+11% order book/sales growth vs FY2019), management’s FY21 outlook (sales of at least SEK27bn) implies 1.6% growth vs FY 19, an extremely conservative guidance given the broad pick-up expected in SWF (in H2 2021) as well as the strong momentum for Betabag (used for sterile transfer) sales (expected to double in FY21).

Margin accretive tailwinds

The recent workplace changes (full remote working option for a large part of its workforce), Getinge should be able to reduce its cost structure further. While the company had guided last year (Q3 20) that about half of the COVID-19 savings were likely to be permanent (2.5-3% of ~5-6% pandemic tailwinds – AV estimate), we believe that the savings could be significantly higher than that. In addition, following a pick-up in consumables (likely in H2 21) and strong Betabag sales (higher margin product), we believe margin expansion should continue in the near term (~1pp underlying margin improvement likely in FY21 – takeaway from CEO comment on the conference call).

Access to fundamental research on GETINGE : click here

Access to GETINGE's ESG scorecard : click here