Whitbread is always worth another look

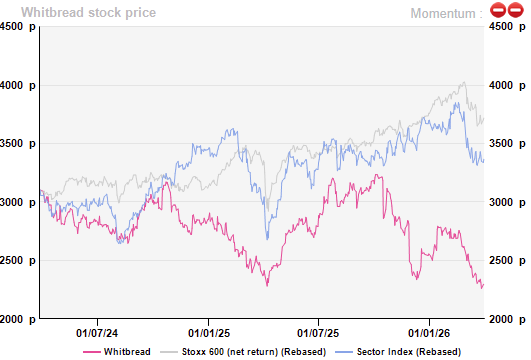

Whitbread’s (BUY; UK) share price has been hesitating over the past two years, from plunging on UK RevPAR softness, before rallying on trading beats, only to fall again following the UK Budget announcement, and more recently amid geopolitical tensions in the Middle East. The end result is that it is remarkably cheap. Whitbread is structurally well-positioned to benefit from an inevitable ‘normalisation’ in travel demand (an oxymoron?), and easing macro conditions.

Clear leader in the UK Midscale & Economy segment

Whitbread UK’s Premier Inn brand, aimed at midscale demand, benefits from strong customer recognition and resilient demand dynamics. Its RevPAR always considerably outperforms that of comparable peers. This operational strength is supported by an industry-leading direct sales channel capturing approximately 99% of bookings, limiting reliance on high-cost third-party distribution channels. The group is a proactive asset manager with the closure or disposal of around 200 of the least profitable branded pubs and restaurants, followed by conversion into hotel sites while freeing up space for approximately 3,500 additional rooms. Another key part of its ongoing expansion is its office-to-hotel conversion strategy, particularly in high-demand urban centres. As the post-pandemic shift in workplace dynamics has led to a surplus of vacant office space, Whitbread's conversion model allows it to secure prime, central locations that would otherwise be unavailable for new builds and shortens the timeline from acquisition to opening.

Together, these measures underpin Whitbread’s ambition to reach approximately 98,000 UK rooms by FY30 (from 86,000 in FY25) and reinforce its dominant market position.

Near-term margin pressure stemming from the UK business rates increase remains a key consideration, particularly given the group’s nearly 90% exposure to the UK market. The direct impact is estimated at approximately £35m in FY27, down from £40–50m initially. Multiple mitigation levers include challenging rateable value assessments and negotiating cost-sharing mechanisms with landlords in leased properties. In addition, consistent delivery on internal cost-saving initiatives has provided incremental efficiency gains, partially offsetting the pressure. Medium term margins at c.22% are at hand.

Germany poised to bring profits

Backed by a solid balance sheet, Whitbread is actively replicating its proven operating model in Germany, a larger but historically fragmented market lacking a dominant national chain leader. The German hospitality sector is characterised by event-driven demand and relatively volatile pricing dynamics, conditions that have historically limited branded penetration. Whitbread’s structured expansion strategy is gaining traction alongside estate maturation, with adjusted pre-tax performance approaching breakeven and profitability expected in FY26 ending February 2026. Room additions in Germany are expected to accelerate from FY27 onwards, with total capacity projected to approach 20,000 rooms by FY30 (from 11,000 in FY25). The scaling of the German platform remains one of the group’s most important medium-term growth drivers, and will promote progressive geographic diversification.

Upcoming strategic revision

The capital requirements associated with the pipeline conversion and expansion plans remain substantial through FY28, reaching levels broadly comparable to the group’s current market capitalisation. Net debt is expected to remain stable in the near term, reflecting the group’s continued prioritisation of shareholder rewards in line with industry practice. While a portion of expansion funding will be sourced through asset disposals and sale-and-leaseback transactions, this approach is likely to result in structurally higher rental expenses over time. The group’s five-year plan is currently under review. We consider it increasingly likely that Whitbread will extend its sizeable investment programme, while maintaining competitive shareholder distributions and gradual deleveraging (adjusted Net debt/EBITDA expected to decline from 4.64x in FY25 to 4.28x in FY28).

Quality governance

Whitbread benefits from an experienced and independent (even under our strict in-house criteria) board, and a 100% free float shareholder structure, supporting transparent oversight and disciplined capital allocation. The presence of activist investor Corvex, currently holding over a 6% stake and seeking Board representation, adds a layer of scrutiny over strategic direction and capital deployment. Corvex has publicly called for a strategic plan review supported by independent external advisors, particularly in light of the challenging UK macro environment.

Management’s constructive reassessment of the five-year plan illustrates a welcome responsiveness to the shareholder voice. The executive team has been led by Dominic Paul, Group CEO since 2023, with extensive industry experience, including leadership at Costa Coffee before the latter’s spin-off from Whitbread. His track record in brand development and operational execution is viewed as supportive of the group’s ongoing transformation ambitions.

Impact of the Middle East conflicts

Whitbread’s direct exposure to the Middle East remains limited, with 3,184 rooms (11 hotels) in the GCC, operated through a 49/51 JV with Emirates, representing roughly 3% of the total group portfolio. Regional demand disruption indeed presents a short-term risk, as illustrated by reports of sharply reduced occupancy levels in certain markets such as Dubai. We have incorporated a modest JV loss into our FY27 projections. Over the medium term, travel demand is expected to revert to pre-war pace. The recent (mid-February) MoU for approximately 3,500 additional rooms in the GCC therefore appears manageable from a risk perspective, given the typical three- to five-year development timeline.

One structural observation remains Whitbread’s asset-heavy operating model, which increases its sensitivity to inflationary pressures. The proportion of owned real estate has risen from approximately 40% to over 50% currently, reflecting weaker investor appetite for sale-and-leaseback structures since the pandemic. As a result, Whitbread remains more exposed to operational cost volatility than asset-light peers, despite in-place hedging strategies and disciplined cost management. War-driven inflation affecting both travel demand and operating costs, particularly energy, mainly gas/electricity (over 80% of anticipated FY27 consumption has been hedged), alongside rising interest rate concerns, represents a clear headwind, although Whitbread may benefit from a reinforced competitiveness during economic downturns given its leadership in the Midscale & Economy segment.

Valuation

Whitbread offers compelling upside potential based on fundamental valuation metrics, supported by a favourable ESG profile. Relative valuation metrics remain mixed, with EV/EBITDA and P/E multiples suffering from short-term earnings compression and elevated investment plans, while the comparatively attractive P/Book valuation reflects the group’s high level of asset ownership relative to predominantly asset-light peers. The group’s continued commitment to shareholder distributions appears broadly aligned with industry capital allocation practices.

For sure, cyclical sectors such as hospitality remain under pressure in the current macro environment. Nevertheless, Whitbread’s dominant position in the UK, disciplined cost management, promising German platform and substantial asset backing make it a low-risk quality investment. Short-term volatility is clearly an entry point for Buy-to-Hold investors

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...