Water Tabs

Water utilities are not anybody’s priority and particularly not so when it comes to the handful of UK ones marred by the Thames Water disaster. The cash extraction driven by Thames Water’s private shareholders were of epic proportions, outfoxed the UK regulator and brought about a lot of negative sentiment on the whole UK water industry. In this dramatic context, United Utilities managed to protect its shareholders (if not its customers), and have actually delivered a very respectable performance over the last 10 years.

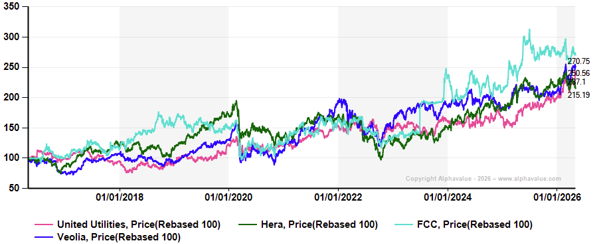

But is this still the case when matched to alternative listed European water utilities? It is, and that has come as a surprise, as it implies that a deliquescent water regulation model has been no brake to wealth creation. United Utilities, Veolia, FCC and Hera have gained about 150% each over the last 10 years, as much as the Stoxx600, dividend included. There are worse businesses.

Same tap water? 4 different countries & businesses, same gains

UU and Hera (Italy, €6bn market cap, multi utility of which water accounts for 20% of Ebitda) are RAB based. The game has been and remains for their managers to find the proper balance between what they can afford balance sheet wise, and what return they can expect through regulated price increases. Both own their assets and are keen to deliver dividends on a steady basis.

Same tap water? 4 different countries & businesses, same gains

UU and Hera (Italy, €6bn market cap, multi utility of which water accounts for 20% of Ebitda) are RAB based. The game has been and remains for their managers to find the proper balance between what they can afford balance sheet wise, and what return they can expect through regulated price increases. Both own their assets and are keen to deliver dividends on a steady basis.

Veolia (French, but a very international public services utility) and FCC (a Spanish old hand, but a newcomer to public services) fall into the concession category. Water services account for a third of FCC’s Ebitda and 48% at Veolia. Concession players do not own the operating assets but will book them as concession assets in their balance sheets. These are meant to be given back to the local authorities when the concession ends. Those assets that are being built in the course of the concession, are also owed to local authorities. Concessions tend to be renewed so Veolia and peers are endless caretakers of third party owned assets. They obviously book associated returns as their own, and should provision handover costs, usually a murky part of the accounts.

Continental public services have been marred by corruption scandals (mostly last century), but have a good record on water services delivery. UK water services are a continuing story of underinvestment and environmental catastrophes, but have not faced serious corruption issues.

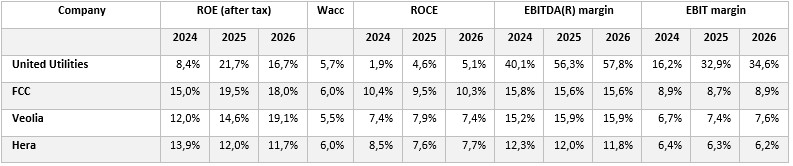

All this being exposed, does it matter for returns? No. Consider the following measures of asset sweating. Remember that FCC is concession based but new to the game. Remember too that UU is the only pure water play in that table.

Financial performances of water related business. 2024-2026

Financial performances of water related business. 2024-2026

What the above table shows is the strong operating performance of UU ending up with only an average ROE. What the table hides is the remarkable volatility of UU’s past returns, with a 2021 negative ROE. In effect, UU is facing a very slow asset rotation (15%), where not such close peers run at 100%. Concession assets are seemingly lighter to bear, but again, the assets of the other 3 are not entirely dedicated to water services.

Due to the diversity of the businesses of the continental players, it is wiser not to push comparisons much further with UU. It looks anyway as if the British player has eventually struck gold in water services. Not an obvious observation.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...