Time to take AI chips off the table

We agree with the still discreet but rising chorus of market participants calling the AI capex a bubble of monumental proportion. The hard truth is well known:

-

AI tokens are sold massively below costs

-

At prices below costs, there are no takers anyway for paid AI services beyond coding

-

There is no hope whatsoever to get a return on the $1tn invested in compute in 2026 alone

-

There are no hard figures provided by the two ‘incumbents’ (Anthropic and OpenAI) while circular funding arrangements put at risk most participants in a daisy chain where only Nvidia prints AI cash flows

-

Nobody in the investment banking community wants to speak the truth as long as the honey from the coming SpaceX IPO and Open AI one has not been cashed in.

Like others, AlphaValue has been dubious of AI economics since circular funding arrangements surfaced, i.e. last autumn. Bulls won, even if the Oracle share price (a compute capacity provider eventually) and its CSDs tell us that the believers are in dwindling numbers.

The initially equity based (albeit circular) funding has turned to debt funding, say $300bn raised over the last 18 months. In other words it stinks.

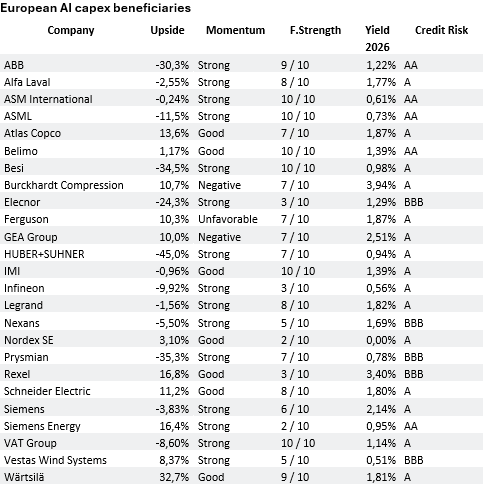

Europe benefitted as a capex provider to mushrooming US datacenters. Last October, AlphaValue had, somewhat skeptically, drawn up a list of 25 stocks benefitting from the demand for AI infrastructure. The list is available below. Here is the performance of that list (equal weighting):

The outperformance was clearly good to have and it is way too early to call it quit.

We would however be increasingly concerned by the collateral effects of the SpaceX mega listing. Money may be needed to chase that pipe dream at the expense of AI type money and investment bankers may speak up their mind more clearly past that date.

That list offers now a -4% fundamental downside. It is time to trim positions.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...