Pernod Ricard: two families, one glass too many

From €120 at our last Teaser to €64 today, the market has spoken : Pernod Ricard (BUY; France) no longer deserves its premium. A shrinking spirits market, a sinking China, a family watching its grip loosen against Brown-Forman, the stock ticks every box of a name to avoid. That is precisely why it interests us. At 11.2x FY26E earnings and a FCF yield of 7.6%, the market is pricing permanent weakness into a group that is restructuring, shedding dead weight, and whose family, if the Brown-Forman deal closes within a French legal framework, has no intention of letting go of the wheel.

I. Same ice, thinner glass

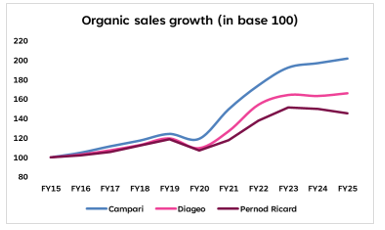

Since our last Teaser in September 2024, Pernod Ricard has kept melting, and this time it is no longer a difficult post-Covid hangover, but a structural shift. What looked like a temporary floor around €120 in August 2024 has nearly been cut in half at €64, levels not seen since late 2006. What read then as a shared sectoral shock, now applies more to Pernod than to anyone else. Diageo (BUY; UK) is suffering too, granted, but the divergence in trajectory between the two has been visible since 2022, while some peers like Campari (REDUCE; Italy) have managed to sidestep it altogether.

The geographic diagnosis from last year still holds : a durably pressured America (-15% organic growth in H1 FY26), a domestic spirits market that remains soft, and a China that keeps sinking (-28% in H1 FY26, with Martell cognac bearing the brunt).

II. Two families, one power struggle

On 26 March 2026, Pernod Ricard confirmed it was in talks with Brown-Forman for a "merger of equals." Behind the polished press release, the reality is rougher : this is first of all a family affair, and the two dynasties need to agree not just on price, but on who runs the combined entity.

The starting asymmetry is striking. At Pernod Ricard, the third generation led by Alexandre Ricard holds around 15% of capital through the Concert Paul Ricard. At Brown-Forman, the fifth-generation controls 67.5% of Class A shares, the only shares carrying voting rights, representing roughly 24% of total capital. The Ricards hold a minority stake in a larger group ; the Browns have a far tighter grip on American voting rights.

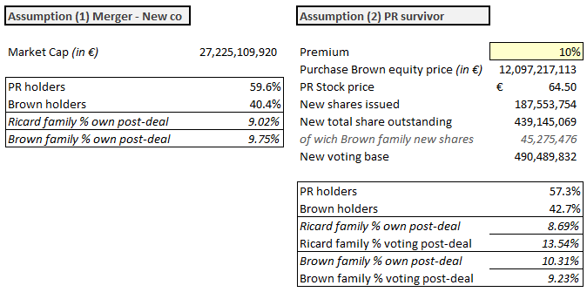

If the deal is primarily structured as a share exchange (as press reports suggest), the resulting dilution would fall squarely on the Ricards. In a scenario where Pernod absorbs Brown-Forman, the Ricard family would hold only 8.6% of the combined capital against 10.5% for the Browns, even though Pernod would represent 56.4% of the group. In a NewCo structure, the gap narrows slightly (8.9% vs 10.0%), but the direction remains the same.

The only lever capable of reversing this arithmetic is the double voting right. Pernod Ricard's bylaws provide this mechanism for any registered share held for at least ten years. In a scenario where Pernod survives as the parent under French law, the Ricard family would control 13.3% of voting rights against 9.5% for the Browns, despite holding less capital. This double voting right exists only within a French legal framework. A NewCo structure, let alone an American parent, would strip the Ricards of it and shift the centre of gravity across the Atlantic.

The market reaction captured this complexity well, proving nothing is settled : Brown-Forman surged on the announcement while the French group dropped (Pernod being Pernod) before partially recovering. For an all-stock transaction, this performance asymmetry makes the "merger of equals" framing hard to sustain. The most favourable structure for the Ricards would be a French parent absorbing Brown-Forman as an American subsidiary, preserving double voting rights while gaining a broader US listing. Any other structure, a neutral NewCo in particular, would be presented as more balanced on paper, but would amount to the Ricards surrendering their main control tool with no guarantee of getting it back.

Beyond governance, the family's financial capacity to rebuild a position in case of dilution is limited. Pernod Ricard has distributed more than its cumulative earnings over 2020-2025 between dividends and cancelled buybacks, pushing up its debt load. The family holding structure's debt could reach €1.6bn, with latent capital gains on the stake limited to €487m at current prices. The double voting right is therefore not merely a political shield, it is the only real safety net left should the deal go through.

III. Reinventing on a shrinking dance floor

Tomorrow 2 is not another cost-cutting plan dressed up with a grand name. It is the end of the "one brand, one organisation" model : two business units, Gold and Crystal, where there used to be as many as there were brands in the portfolio. The real test for the Marseille-based group will come in 18 months, not in the cost line or the announced €1bn in savings, but in the conversion of EBITDA into FCF. And that conversion is starting to show some colour : €853m in FY24, €1,066m in FY25, €1,236m expected in FY26.

The portfolio rationalisation follows the same logic. Where our 2024 Teaser counted 2 disposals against 5 acquisitions, the trend has since reversed : 7 disposals for only 3 acquisitions since our last Teaser. The group is finally shedding what was dragging it down. What remains must grow, and that is precisely where the shoe still pinches : a leaner group is not necessarily a growing one.

The harder problem is that Pernod is reinventing itself in a shrinking market. Generation Z drinks less than its predecessors, GLP-1 drugs are starting to weigh on consumption behaviours, and the premiumisation that masked flat volumes for a decade is hitting its ceiling. Pernod is restructuring against a contracting backdrop, a very different equation from 2015.

The new architecture can work, but only if it executes faster than its peers. The consumer shift is clear : aperitif is the new digestif, and large premium formats are losing ground to convenience formats. Campari saw this coming a decade ago with Aperol ; Pernod is catching up with Italicus and St~Petroni. Right direction, but Campari had a ten-year head start and the results to show for it. Pernod cannot afford to miss another step.

RTDs remain the only credible near-term growth relay, up +20% in the US while hard seltzers decline 7.4%. But let us keep perspective : 2% of North American sales today. A real growth driver, but not a meaningful earnings contributor before FY28 at the earliest.

IV. Priced for extinction, built to last

At these levels, Pernod Ricard looks more like a de-rated name than a broken one. Valuation has compressed sharply, with adjusted P/E falling from 27.8x in FY24 to 11.2x in FY26E in our model. Cash is holding up better than market sentiment suggests : pre-dividend FCF climbs from €0.85bn in FY24 to €1.06bn in FY25 and would reach €1.24bn in FY26E, implying a FCF yield of 7.6%. A dividend yield of 6.9% in FY26E further suggests that a large part of the bad news is already in the price.

The thesis ultimately rests on a simple conviction : the Ricards will not abandon ship. Three generations of building do not end in a quiet dilution inside an American NewCo. The balance sheet leaves less room than before, with Adj. Net debt/EBITDA at 3.40x in FY25 and 3.88x in FY26E, limiting flexibility if Brown-Forman would be poorly structured. However, if the family opts to preserve the French framework and the double voting right, as their entire history suggests they will, then Brown-Forman becomes a catalyst rather than a threat.

With a restructuring that was long overdue, a leaner portfolio positioned to capture the right trends, and a family whose interests remain aligned with minority shareholders over the long term, the market is pricing a centenary family business as if it were about to disappear. It is not heading that way. At this price, that is an invitation to enter.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...