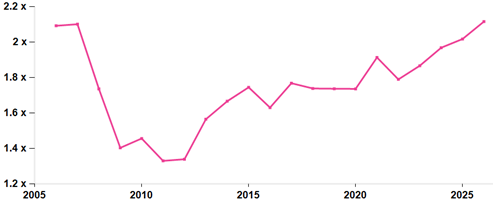

P/Book unimpressed by Hormuz

At pixel time the average P/Book 2026 ratio for the AlphaValue coverage universe is a cool 2.1x. This is as brisk as 20 years ago when things eventually blew up in the GFC fireworks.

20 years of European P/book (average for past years, spot for 2026)

A closer view of recent 2026 P/Book development confirms that bulls are in charge. The Iran war hit has been short lived. Investors’ liquidity seems never to dry up, with dips still considered as points of entry.

2026 P/Book – 1 year

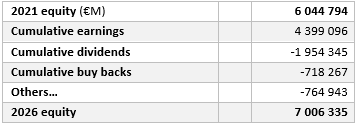

The steady rise of the average P/Book between 2021 and 2026 is partly owed to the rather modest progress of the book side of the calculus. The equity base has increased by 17% over the period when the corresponding market cap gained 30%.

Here is the bridge between 2021 and 2026:

In effect European equities paid out 61% of their earnings over the 2021-2026 period. To some extent European equities are looking like a giant Imperial Brands: they pay out a lot as they find it so difficult to dig for growth. Banks are no small contributors to this state of affairs, as they have paid out c. €525bn over this time span, or about 19% of total returns to shareholders.

This is certainly a provocative summary view, but raises the perennial question of whether paying out a lot is right. In a chicken and egg situation, investors in European equities go for the cash now and growth later because they know that the current stable of European equities is made of mature businesses.

As long as liquidity is ample, European equities may well continue to pay out more, and be more highly valued from a P/Book standpoint.

This nice music has stopped playing at Imperial, incidentally.

Subscribe to our blog

AlphaValue's Fundamental Strength Indicator reveals 24 "unsinkable" business mo...

A $330 share price, 40x earnings expected five years from now, and growth funded by SoftBank: wh...