Flutter

Note: This is a daily stock update and the information stands true as of 26/09/24, 09:00 CEST.

Company Update:

As a part of its capital markets day 2024, Flutter unveiled new mid-term targets through 2027 and also announced plans for a huge $5bn share buyback program.

The firm expects 2030 regulated TAM of $368bn (o/w $70bn from the US and Canada; $298bn from ROW), translating into a 8% CAGR in global gross gaming revenue (GGR) with online penetration estimated at 43%. In addition, the unregulated market is estimated at c. $210bn (~57% of the regulated market size).

These estimates underpin the firm's ambition to reach $21bn in revenue by 2027, representing a 3Y CAGR of 14% (well ahead of market) and adjusted EBITDA in 2027 of over $5bn (margin expansion of ~700bps). Further, the firm forecasts free cash flow generation of approximately $2.5bn in 2027, a forecast 36% CAGR, which enables the ambitious $5bn share buyback program, which will be launched in November 2024, and will run over the next three-four years.

The new guidance implies a mid-to-high single digit upgrade to consensus estimates. We will revise our estimates by high single digits to factor in the solid mid-term outlook.

Expert Opinion:

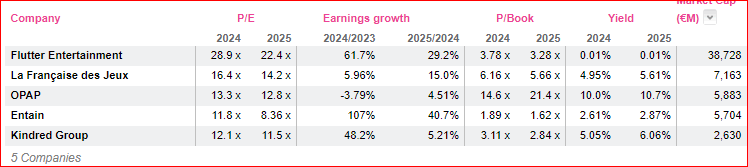

These are very strong numbers that will prompt us and the consensus to upgrade their numbers. The momentum remains very strong and is undeniably a high quality name in the sector. I believe there is substantially better risk reward profile on Entain (Gaming, Buy, £5bn mkt cap, 100% upside) where we believe the momentum is set to improve (and actually started to improve in Q2 with better guidance for the rest of the year.

For daily updates, subscribe to our newsletter and for detailed daily updates, reach out to us at sales@alphavalue.eu

Company Update:

As a part of its capital markets day 2024, Flutter unveiled new mid-term targets through 2027 and also announced plans for a huge $5bn share buyback program.

The firm expects 2030 regulated TAM of $368bn (o/w $70bn from the US and Canada; $298bn from ROW), translating into a 8% CAGR in global gross gaming revenue (GGR) with online penetration estimated at 43%. In addition, the unregulated market is estimated at c. $210bn (~57% of the regulated market size).

These estimates underpin the firm's ambition to reach $21bn in revenue by 2027, representing a 3Y CAGR of 14% (well ahead of market) and adjusted EBITDA in 2027 of over $5bn (margin expansion of ~700bps). Further, the firm forecasts free cash flow generation of approximately $2.5bn in 2027, a forecast 36% CAGR, which enables the ambitious $5bn share buyback program, which will be launched in November 2024, and will run over the next three-four years.

The new guidance implies a mid-to-high single digit upgrade to consensus estimates. We will revise our estimates by high single digits to factor in the solid mid-term outlook.

Expert Opinion:

These are very strong numbers that will prompt us and the consensus to upgrade their numbers. The momentum remains very strong and is undeniably a high quality name in the sector. I believe there is substantially better risk reward profile on Entain (Gaming, Buy, £5bn mkt cap, 100% upside) where we believe the momentum is set to improve (and actually started to improve in Q2 with better guidance for the rest of the year.

For daily updates, subscribe to our newsletter and for detailed daily updates, reach out to us at sales@alphavalue.eu

Subscribe to our blog

Alphavalue Morning Market Tip

The US struck 80 sites in Iran and revoked Iran's general license to sell oil.